TELLER MACHINES

by Candice Zarr

Candice Zarr is a computer consultant and technical writer for the Chase Manhattan bank.

Across the nation, possession of the right plastic card (and a usable bank balance) is easing the long-lines trauma usually associated with banking. Now your relationship with your money can be fluid and convenient with the automated teller machines (ATMs) that allow immediate access, twenty-four hours a day, 365 days a year, to funds in your checking, savings and money market accounts.

Each bank has its own ATM system, but certain features are common to all: an account, an access card and an ATM. The standard cash machine looks like a panel inset into a wall. The panel usually contains a screen on which the ATM displays messages, a keyboard, and slots for access card insertion, withdrawals and deposits.

Those bright lights and all that shiny chrome may infrequently cause a case of computer jitters, but ATMs are designed to be practical, easy and, some say, fun to use. They are user-friendly in English, sometimes in Spanish, and they rarely make a mistake. To perform most standard banking transactions, all you do is press appropriate keys on the keyboard in response to menu-style lists of choices.

Twenty years ago ATMs existed solely in the minds of researchers and executives at Howard Savings Bank. After a demonstration of the nation's first commercial on-line reservations system at American Airlines, the executives at Howard Savings concluded that if it could work for reservations and people, it could be modified to work for savings transactions and depositors.

Soon the Savings Automation System was introduced by a firm called eleregister, and shortly thereafter IBM, Burroughs and all the rest came out with their own systems. But back in the 1960s most commercial banks showed little enthusiasm toward their savings operations. Not until the convergence of a number of factors-the expansion of branch banking, technological advances that improved cost effectiveness, and the growing desire of bank management for a way to integrate customer information-did a strong push for the adoption of full-capability on-line teller operations get under way.

Around 1972 designs for teller systems began to look more like what we recognize as "standard" ATMs when Bunker Ramo introduced the Universal Teller Terminal, consisting of a keyboard, display screen, journal tape and validation printer all in one unit. By 1974 improved systems comprised minicomputer-based, programmable control units that served as terminal controllers and communicators, and provided calculating capability at each branch.

Cash on Demand

Today's systems are designed to be used by those of us who have had no previous contact with computers, yet while using an ATM we are in communication with a large mainframe computer somewhere across town. The ATM acts in the manner of a computer terminal connected to the bank's main system. When the access card is inserted, the ATM initiates communication over a network of communications lines dedicated just to this purpose.

After the machine has provided an on-screen greeting and made sure you are who you say you are (by a process we'll get into a little further on), it will display its "menu" listing of the transactions you may perform. By pressing one of the keys located alongside the various options, you may find out your balance, transfer funds from one account to another, make deposits or loan payments, or-and this is the feature that has endeared the machine to millions-request and receive cash.

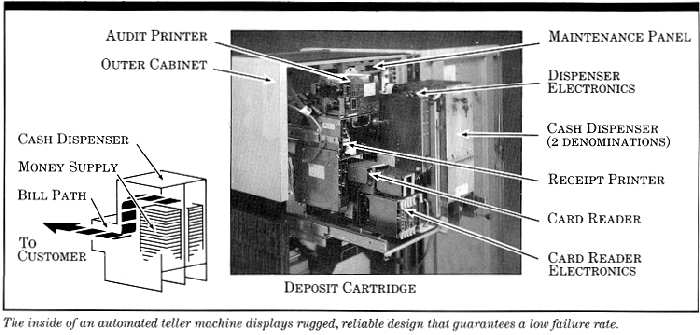

Let's look inside your average ATM. From the outside you see a shiny panel with an inset display screen and several slots for deposits and withdrawals. From within the bank you would see a door with combination and key locks, similar to the big vault door guarding your safe-deposit box; beyond the door you would see a vault box connected to the deposit slot for collecting deposit envelopes. You would also see a device containing locked "cassettes" of ten- and twenty-dollar bills for dispensing cash.

When you tell the ATM that what you'd really like is fifty dollars, the ATM first calculates the ratio of tens to twenties on hand to avoid running out of one denomination. The appropriate bills are fed up to an optical scanner, which checks the length, breadth and height of each bill before it is passed out to you. Bills that appear defective are set aside in a special bin.

Once your transactions are completed, a small printer records what happened onto a receipt tape and feeds it through a separate slot at about the same time that your card is returned to you. At this time, on most systems, communications between the ATM and the host computer are severed, thus safeguarding your records and your money.

The Safety Factor

Just how well protected is your money? Oddly enough, you are one of the weakest links in this regard. Generally, when you get your access card, you are asked to come into the bank to pick a number. This number, called a PIC (personal identification code), is typed by you into a special terminal and from that time on is known only to you and the central computer. Nobody at your bank can access the number. When you enter it into the machine, the screen will print only a row of asterisks (****). Access to your personal code is so secure that if you happen to forget it, you have to come in to pick a new one.

The magnetic stripe on the back of your card contains three lines of binary information, giving your name, your card number and just about whatever you can read on the front of your card. When you feed your card to the machine, this information identifies you to the ATM. The main system will request your PIC as additional identification, then compare what you punch in with what the file contains. If they match, you are awarded access to your accounts. If they don't, the system will disgorge your card. Repeated failures may trigger the system to swallow the card under the assumption that someone may be trying to get unauthorized access to your money.

Should you want to make a deposit, you enter on the keyboard the amount and type of deposit, then insert an envelope containing cash, checks, deposit slips, etc., into the deposit slot. Yes, you can deposit cash. Your deposits are enclosed in a vault constructed to withstand impacts of up to fifty thousand pounds per square inch. Should there ever be an attempt on the ATM itself, doors automatically lock and microprocessor-based alarm systems notify a central security monitoring point. There are even heat-sensing devices around the body and chest of the ATM.

Banks select their ATM sites with an eye to high traffic, bright illumination and safe surroundings. Indoor ATMs are typically enclosed by glass or transparent material. While this does afford protection for the machine itself (who would try a break-in where they can be easily observed?), it can be somewhat unsafe for customers. The customer and his withdrawals are "in the spotlight" when seen from the street, and they may unknowingly be observed and followed. For your protection, some banks supply direct-line telephones to customer service representatives around the clock. If need be, they may be used to summon help.

Customers with limited withdrawal capability ($200 to $500 per day) are rarely the targets for robbery. Most frequently it is the service staff who collect and distribute cash to the machines. By servicing machines on a random basis the armed staff significantly reduces the possibility of robbery.

The banks are admittedly confounded by a new, indirect form of theft: "data communications compromise." As the ATM and the host computer exchange authorizations and other commands, messages can be vulnerable to manipulation. Most cases of compromise have been traced to knowledgeable personnel with access to the system. For this reason, completion messages are employed to close the communications loop between the ATM and the host, as well as message coordination numbers and data encryption.

The ATM and its data transmission are relatively safe in comparison with the largest security problem: people. Customer fraud and internal theft are the hardest things to prevent. Modern ATM systems maintain a complete audit trail of everyone with access and everything done on each ATM. While you may look upon this as an invasion of privacy, remember it if you ever have a dispute with the bank. Oh yes, and save those printed receipts. If you're not in the mood to collect paper, you may want to tear up those receipts: they do contain your account number and other confidential data that could fall into the wrong hands.

Occasionally, so many customers are using a bank's ATM facilities at once that the response time degrades. Some systems contain self-monitoring equipment that will notify an operations staff to bring more of its computing and/or communications facilities on-line. The communications network is usually configured in redundant paths: if any part of the system fails, the ATM transmissions can be routed on an alternate path to the host computer. At most sites where there are two or more ATMs, each ATM probably communicates along different paths to ensure availability. Some people resist the idea of using teller machines because of the perception that they are dehumanizing. The notion is that ATMs are part of a grandiose plan to turn us all into proles, grubbing our way through daily banking transactions without ever getting a smile from a friendly teller. If you could somehow convince a teller to go to work at three in the morning, chances are he wouldn't be smiling, anyhow. When New York's Citibank tried to limit live teller access to large depositors, public outcry quickly forced them to rescind this policy.

Modern ATMs help keep the cost of banking down and may stop those charges on your monthly statement from rising. Since there is less paper to be mistyped, mislaid or mutilated, ATMs may provide more accurate banking records than do their human counterparts.

In newer ATM systems, where the access card has a visible magnetic stripe on the back, other cards, such as your Visa or MasterCard, may be used to draw cash advances. This capability is not completely widespread (check with your bank). The older systems, with the magnetic stripe embedded into the card, can't do this-one of the penalties for being the first kid on the block to go computerized.

Banks are experimenting with different forms of bank-at-home systems, using personal computers and modems. Some people think this system will be the wave of the future and could make ATMs obsolete. But until we can train our personal computers to disgorge twenty-dollar bills on command, ATMs will still be around.

Return to Table of Contents | Previous Article | Next Article